To cushion the volatility of the dollar and international indexes, the FEPC was created to introduce a regulated price, which every month would move - maximum - 2.8% in either direction, seeking to approach - slowly - the international price. In principle, the fund was to be self-sustaining, since, in times of low international prices, the regulated price would be above - generating a surplus for the nation -, while, in times of high prices, the regulated price would be below - generating a deficit.

To cushion the volatility of the dollar and international indexes, the FEPC was created to introduce a regulated price, which every month would move - maximum - 2.8% in either direction, seeking to approach - slowly - the international price. In principle, the fund was to be self-sustaining, since, in times of low international prices, the regulated price would be above - generating a surplus for the nation -, while, in times of high prices, the regulated price would be below - generating a deficit.

In analyzing the data, however, significant challenges could be foreseen. In particular, when international crude oil prices fall sharply, the peso tends to devalue at a similar rate. This negative correlation dampens the impact on the international price, causing times of low prices to generate a small surplus. However, when prices rose rapidly, the effect on the peso was small, so that the deficit was

significant. Thus, the movements of 2015-2016 and 2020-2021 led to significant deficits that today have the FEPC with historically low prices.

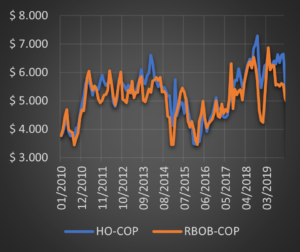

With the elimination of the regulated price, new challenges are coming for the country's fuel consumers (particularly the transportation sector). In particular, looking at the 2015-2016 period, as in the figure above, the price in pesos has been little volatile in the face of the drop in oil prices in 2015, because it was accompanied by a 50% devaluation of the exchange rate.

Today, however, we are experiencing significant growth that has not been accompanied by the expected revaluation in exchange rate (although in dollars, today the price is at comparable levels with 2018).

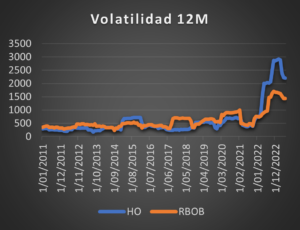

A natural way to measure the effect is the volatility of monthly changes, which could be interpreted more intuitively as what would be a "normal" movement in a month. During 2011, monthly volatility hovered around COP$300-COP$350, while today that value is at COP$2000. In other words, if before a normal month, the price of gasoline or diesel could move about COP$300 per month, today a normal movement would be COP$2,000 per month. This represents the negative side of linking ourselves to the international price: even in times of greater calm, we could be anticipating movements of $300 every month (in either direction), while in times of stress, we should not be surprised by movements of $2,000.

A natural way to measure the effect is the volatility of monthly changes, which could be interpreted more intuitively as what would be a "normal" movement in a month. During 2011, monthly volatility hovered around COP$300-COP$350, while today that value is at COP$2000. In other words, if before a normal month, the price of gasoline or diesel could move about COP$300 per month, today a normal movement would be COP$2,000 per month. This represents the negative side of linking ourselves to the international price: even in times of greater calm, we could be anticipating movements of $300 every month (in either direction), while in times of stress, we should not be surprised by movements of $2,000.